The post-WWII era is coming to an end. Its most taken for granted institutions, (e.g., the US dollar, NATO, IMF, etc.) and ideologies (globalization, neo-liberalism, etc.) have come under stress, and I take the advent of tea as another sign of the growing Chinese/Asian influence. Such signs can give us an idea-set about one of the directions the world may go into. Our own history, in the western market democracies, that is, gives the complementary directions.

It is not easy to foretell if, let alone how, the world turns Asian. If the capitalist model of growth, based on credit, fiat money and inflation, proves to be irresistible, the Chinese still need to put a lot of work into building up a worldwide financial system, with rules and institutions. This kind of work takes decades and/or catastrophic event(s) to bear fruit. The attractiveness of the Chinese economy in a capitalist scenario consists of its being able to theoretically contain larger bubbles than the rest of world. In fact, the world seems headed into a hyper-capitalist direction where countries assemble in blocs and the individual economic entities grow even more. On its current iteration, the EUro bloc stumbled by being just as resilient as its most exposed economy. If the EUro picks up steam again, the US will have to count its friends and integrate accordingly.

From the western history lessons , one should be reminded, if not told, that market democracies had gone through at least one crisis, similar to the one started in 2008, in the beginning of the 20th century, when the international and national versions of socialism looked like better alternatives to the capitalism that worked for fewer and fewer at the expense of most. Communism and Nazism, those being the two versions of socialism introduced above, had their constituencies even in Britain, still the bastion of capitalism at the time--in fact, there were even top royal British figures flirting with Nazism, while Churchill, the ever ideologically-swinging opportunist, found a vocation in opposing Nazism.

In an economical system predicated on limitless growth, problems on the home front start brewing when the system relegates the willing and educated to un/under-employment. Lack of labor competitiveness can work as justification for only so long before these educated folks give ideological shape to the general dissatisfaction with neo-liberal globalization (e.g., trade liberalization, exchange rate controls, and tax-free flow of money). The western elites (aka 1%) are fully aware of all this, and the never-ending war on terror is just a cover for how far the elites have been willing to go to defend the status qvo ante 2008. Another means to counter the emergence of an opposition to neo-liberal globalization is to quickly consider any alternative as enemy of civilization--you know the usual suspects, extremism, nationalism, socialism, totalitarianism, isolationism, etc.

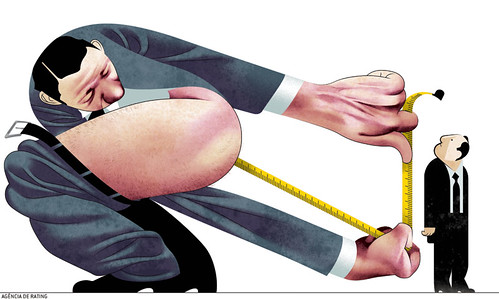

Also, the S-Ir(i)anian diversions can only take us on collision (or is it collusion?) course with China and Russia. While the Russians have been neatly folded in the world system, and the Chinese have risen within the world system, they show signs of nervousness about their positions relative to the hegemon. Strictly on military terms, the US is still ahead, but otherwise, the defection of Germany and/or Japan to side with the challengers can signal continental shifts. Collision is therefore likely to take place through proxies, whereas collusion would give the challengers first right of refusal over certain places on Earth. Of course, the challengers ought to also face their own internal problems--the Russians have to learn how to live with lowering commodity prices, whereas the Chinese are not anywhere close to having developed a viable growth model/alternative at national scale, let alone planetary scale--but then again, who's gonna call their bluff? The existing credit rating agencies and/or Basel III type of capital requirements... or rather plenty of regional conflicts to the effect of Brzezinskian creative volatility.

To return to the US, the bromides of eventually operating markets, be those economic or political, are wearing thin. In fact, markets are social constructs that need constant oversight under the guidance of whatever socially accepted principles. There is nothing intrinsic to markets that prevents the capitalist excess on its way up or down; markets make only a nice abstraction behind which the few tax the most with impunity. Meanwhile, the US academics, busying as usual with minute correlations, are still to catch up with the enormity of the task. One of the difficulties is the epistemological bias against systemic, or ecological, treatment of the problem. Time for change in the ivory towers will come as the higher-ed bubble may lose some air given the job market difficulties of the ever more indebted graduates. However, Americans overall are catching up--a search by "crisis economics" on Amazon.com yields 57,557 results as of this writing.

So, what seems sensible to do? The Occupy movements and the libertarians are just too conceptually fragile to make any progress, given how time changes things. A locally verified solution of the capitalist excess would be something akin to the New Deal. Rather than plunge ourselves down the spiral of destitution and despair for not having a Steve Jobs among each fifty-thousand of us, we could stop thinking in terms of labor competitiveness on a global scale for as long as the jobs match the skills and the fruits of labor enable the best of us to take the whole economy to the next level up. Turning a blind eye to the under-educated immigrants can only depress incomes of the locals, preventing most American children from becoming the next Steve Jobs. Also, good healthcare and education ought to be human rights, not a matter of personal income.

Another new deal requires that the American elite adopt a historically informed perspective, which the current generation of leaders is found missing. There are also notable exceptions, such as Felix Rohatyn, of course, of a different generation, whose 2009 book offers a blueprint that's workable within the current system.

| MINQI LI pdf |

Please note that Minqi Li indicates that the planet may not sustain a bubble tea, regardless of the capitalist logic of the global investor.

19 comments:

I should probably take the time to explicitly credit André Carrilho for his outstanding images. André is a most talented illustrator, who couples a sure hand with a sharp mind. See more here: http://www.andrecarrilho.com

I had hoped this would be a hopeful book somehow laying out a convincing argument that China's rise will eclipse the disintegrating international capitalist economy and usher in a new world order focused on meeting human needs in an environmentally sustainable manner. Sadly, that is not this book's argument.

"Chinese socialism was the historical product of a great revolution, which was based on the broad mobilization and support of the workers and peasants comprising the great majority of the population. As a result, it would necessarily reflect the interests and aspirations of ordinary working people. On the other hand, China remained a part of the capitalist world-economy, and was under constant and instance pressure of military and economic competition against other big powers. To mobilize resources for capital accumulation, surplus product had to be extracted from the workers and peasants and concentrated in the hands of the state. This in turn created opportunities for the bureaucratic and technocratic elites to make use of their control over the surplus product to advance their individual power and interests rather than the collective interest of the working people. This was the basic historical contradiction that confronted Chinese socialism as well as other socialist states in the twentieth century."

The author, Minqi Li, was a member of the student dissident movement of the 80s in China. He describes the milieu during which he studied neoclassical economics at Beijing University: "The 1980s was a decade of political and intellectual excitement in China. Despite some half-hearted official restrictions, large sections of the Chinese intelligentsia were politically active and were able to push for successive waves of the so-called 'emancipation of ideas' (jiefang sixiang). The intellectual critique of the already existing Chinese socialism at first took place largely within a Marxist discourse. Dissident intellectuals called for more democracy without questioning the legitimacy of the Chinese Revolution or the economic institutions of socialism.

After 1985, however, economic reform moved increasingly in the direction of the free market. Corruption increased and many among the bureaucratic elites became the earliest big capitalists. Meanwhile, among the intellectuals, there was a sharp turn to the right... The politically active intellectuals no longer borrowed discourse from Marxism. Instead, western classical liberalism and neoliberal economics, as represented by Friedrich Hayek and Milton Friedman, had become the new, fashionable ideology."

A turn towards neoliberalism had, by the 1980s, been made possible by decades of Maoist development policy, which had developed "the necessary industrial and technological infrastructure [allowing China to] become a major player in the global capitalist economy." Li does a good job explaining the capitalist world-system, according to Immanuel Wallerstein's formulation, with its separation into core, semi-peripheral and peripheral states. The international division of labor has core states, like the U.S. and Japan, performing cutting-edge production requiring massive investment and organization, and which offer the greatest profit margins; the semi-peripheral states, like South Korea and most recently China, performing second-generation production that was cutting edge decades ago but which still offer substantial profits; and the peripheral states, like Angola and Bangladesh, which perform low value-added production like raw material exports and low-tech manufacturing.

Li argues that China's move from peripheral to semi-peripheral status (as China now produces all sorts of high- and low-tech products for the core states) signals trouble for the capitalist world-system: "the current 'rise of China' as well as the 'rise of India,' could be the signal that the capitalist world-economy is calling upon its last strategic reserves (such as China, India, the remaining resources, and the remaining space for pollution) to make one more attempt to jump-start global accumulation... The current global development is likely to suggest that several secular trends, which result from the inherent laws of motion of the existing world-system, are now reaching their historical limits."

Why? Because the capitalist world-system relies on strategic reserves of labor that can be called upon when existing labor forces begin to successfully fight for higher wages. Since the system needs high profit margins to reproduce itself via investment, and since high wages put pressure on profit margins, the capitalist world-system needs countries like China and India to turn to for their cheap labor forces once wage costs, or lack of effective demand (in other words, low wages that reduce a market's buying power) begin to threaten profitability. But the very process of exploiting labor in China - building factories and creating an urban working class, moving China from peripheral to semi-peripheral status - threatens to undermine the ability to exploit such labor in the future. Li explains: "To the extent that the non-core states have lower levels of proletarianization, workers tend to be less educated, less effectively organized, and under constant pressure to compete against a large rural reserve army [of laborers]. The workers in these states, therefore, tend to have much lower bargaining power and receive significantly lower real wages. *The low real wages in the periphery and semi-periphery make it possible for the world surplus value to be concentrated in the core and help to keep down system-wide wage costs*. However, in the long run, the development of the capitalist world-economy has been associated with the progressive urbanization of the labor force. After some initial disorientation, urbanized workers have invariably struggled for higher degrees of organization and extension of their economic, social and political rights. Their struggles have led to growing degrees of proletarianization within the capitalist world economy." (emphasis added)

This spells trouble for the world-system, since as production costs increase in China as workers successfully fight for higher wages, there will be few alternative states for producers to turn to for cheap, educated labor and efficient infrastructure. Also, China's ever-increasing contribution to environmental degradation threatens to undermine the world economy through destruction of the natural environment of which it is a part.

Li's analysis of economic - and, more depressingly, ecological trends - leads to the following conclusion: "With the decline of the US hegemony (reflected by its ever-declining ability and willingness to pursue the system's long-term, common interest), no other state is in a position to replace the US and provide effective leadership for the system. China and every other potential hegemonic candidate all suffer from insurmountable contradictions and weaknesses. None has the ability to offer 'system-level solutions' to 'system-level problems.' Either the existing world-system has exhausted its historical space for potential new leadership and therefore is doomed to systemic disintegration, or the new leadership will have to assume the form of an alliance of multiple continent-sized states, which will then become a world-government and therefore bring the existing world-system to an end.

The capitalist world-economy rests upon the ceaseless expansion of material production and consumption, which is fundamentally incompatible with the requirements of ecological sustainability. Depletion of material resources and pollution of the earth's ecological system have now risen to the point that the ecological system is on the verge of collapse and the future survival of humanity and human civilization is at stake.

To summarize, multiple economic, social, geopolitical, and ecological forces are now converging towards the final demise of the existing world-system, that is, the capitalist world economy."

What comes next could be a rational world-system of production geared towards first fulfilling human needs, then wants, in an ecologically-sustainable manner. But while the current system's demise is assured, there is no guarantee of the character of its replacement, and, at this point, very little likelihood it will resemble the description above.

on Rohatyn's book, 'Bold Endeavors: How Our Government Built America, and Why It Must Rebuild Now'

Felix Rohatyn starts this fascinating book, "The nation is falling apart - literally. America's roads and bridges, schools and hospitals, airports and railways, ports and dams, waterlines and air-control systems - the country's entire infrastructure - is rapidly and dangerously deteriorating."

Levees failed to hold New Orleans' floodwaters, a Minnesota bridge collapsed during rush-hour, three-quarters of America's school building are outdated and inadequate, more than a quarter of its bridges are obsolete or deficient, and half the locks on its waterways are obsolete. The American Society of Civil Engineers estimates that the USA needs to invest $1.6 trillion in the next five years to make America's infrastructure safe.

He shows how large-scale public investments have worked in the past: the Louisiana Purchase; the Erie Canal; the transcontinental railroad, Land Grant colleges and the Homestead Act - all backed by Abraham Lincoln; the Panama Canal; FDR's Rural Electrification Administration and Reconstruction Finance Act; the G.I. Bill; and the interstate highway system.

Rohatyn argues that the USA needs a National Infrastructure Bank to select, finance and manage the needed investments in infrastructure. "America needs to rebuild its infrastructure. It is a critical national priority, a costly long-term investment, and a visionary enterprise. It is a program that can provide tens of millions of much needed jobs. And it is an undertaking that can only succeed if it is directed, coordinated, and largely financed by the federal government."

on Rohatyn's book

"Bold encounters" tells of ten large and transformative public initiatives in American history, often unpopular at the time, but later proven visionary. Those included are the Louisiana Purchase - doubled the size of the country, the construction of the Erie Canal - opening a water route to the West, Lincoln's strong support for the transcontinental railroad, creation of Land Grant colleges and the Homestead Act, building the Panama Canal, bringing electricity to rural America, the G.I. Bill, and creating the interstate highway system.

The underlying purpose of "Bold Endeavors" is to present an urgent call to rebuild America's infrastructure - roads and bridges, schools and hospitals, ports and dams, water, sewer, and electric lines. The American Society of Civil Engineers estimates that $1.6 trillion will be needed to make our infrastructure dependable and safe. Doing so will also create tens of thousands of new jobs, and reduce the estimated 13,000 deaths attributed to poor highway maintenance.

Rohatyn contends that the ten stories in this book demonstrate that large-scale public investments can work, and with remarkable long-term success.

The federal government is spending $73 billion/year on infrastructure, without a system to objectively prioritize. Rohatyn proposes a National Infrastructure Bank to both issue bonds for their funding and to rank proposals. Interestingly, Rohatyn, a former Wall Street investment bank leader, also believes that these problems are due to investment having been replaced by speculation, and that capitalists are killing capitalism.

Finally, Rohatyn reminisces on his earlier service helping New York City avert bankruptcy - unfortunately, irresponsible leadership since then has brought the problem back through overly generous funding of public employee wages and retirement benefits. Meanwhile, China is investing $200 billion in railroads over 4 years, starting in 2006.

This year, investors have been gobbling up US treasuries in a desperate effort to search for safety. But would they have done better to grab Australian sovereign debt or Singaporean bank bonds, as a shield against political incompetence in a fractious world?

If the wealth management arm of Merrill Lynch is to be believed, the answer could be “yes”. This month, the US broker is quietly circulating a memo which tells its affluent clients to reposition themselves – and their portfolios – for a fundamental

geopolitical shift.

During much of the late 20th century, the broker says, the world was shaped by American-dominated institutions, such as the Group of Seven wealthiest nations. But during the financial crisis of 2007 and 2008, it became clear western dominance was crumbling, and the focus moved from the G7 to the G20, which includes emerging markets such as China. But now the G20 is looking impotent too; thus the world is trapped in a scary limbo. China and the other emerging powers are wary of taking a leadership role, but the west is declining. The net result then, is that nobody is in charge; it is an unstable “G-zero” world, to use the phrase posited by Ian Bremmer, the political consultant.

Merrill Lynch is trying to tell its clients how to respond (other than panicking and burying gold in the ground). It suggests, for example, investors should put money into companies, not governments, since the former are more reliable,

transparent and growth-orientated. It calls for a rethink of the traditional binary distinction between “developed” and “emerging markets” countries; the latter includes some countries (such as Ghana and Indonesia) which are likely to flourish for structural reasons, but others which are not.

It recommends buying exchange-traded funds (ETFs), to guard against the inflation and sky-high taxes that it fears will be unleashed by desperate governments. And the US broker says it is time to abandon the idea that treasuries are a special asset

class, let alone “risk-free”; this no longer makes sense in a G-zero world. “Unlike old US-centric portfolios that called for nearly half of bond allocations being dedicated to US treasuries and municipals, [our] current models consider all bonds

“global”,” Merrill Lynch says. Hence that interest in Australian sovereign debt or Singaporean bank bonds.

Now, Merrill Lynch is certainly not the only broker currently exploring these ideas. And not everyone will agree with the details of this survival strategy. (I always get suspicious when brokers start flogging ETFs, since they get fees if investors buy these products, rather than burying gold.) But if nothing else, this memo is an intriguing sign of the times, on several levels.

After all, a decade ago, when investors tried to decide where to allocate their cash, they typically did so by crunching through macroeconomic numbers. These days it is becoming clear that the crucial issues for the global economy cannot be plugged into a spreadsheet. This shift is scary in itself for investors, given that most were trained to handle hard numbers, not vague issues such as political culture. What is doubly unnerving is that western politics is not behaving as we think it should. The years after the second world war were not just a period when the G7 ruled; there was a presumption that politics should be imbued with a positive vision and sense of mission, whether national or local. So, 70 years ago, the west created the Bretton Woods system, and 16 years ago, at the height of the Asian financial crisis, journalists quipped there was a “Committee to the Save the World”, or an informal group of US policymakers trying to quell the crisis.

But today, as Merrill Lynch notes, there is no dominant bloc or power; nor (though the broker does not spell this out) is there vision or mission.

Inside the US, politicians still cite the American dream; but no one today quips that US leaders could form a “committee to save the world”, or even the eurozone, And in Europe, politics is being driven not by any positive vision, but a terror of collapse. Fear, not mission, is the order of the day. Rarely has politics seemed so crucial for investors, and yet so impotent. The craft of government has become defensive,

reactive, small-minded and profoundly frustrating to watch. If you doubt this, consider those endless eurozone summits or American fiscal debates.

And yet, what the Merrill Lynch note shows is that some financial players are now trying to adapt: rather than endlessly dreaming of a new “solution” (to the eurozone or anything else), some asset managers are now adjusting to an era of grinding instability. In some senses,

this is profoundly depressing; but in other senses, this process of adaptation may offer a crumb of cheer. Or at least it does if you are a

Singaporean bank that now wants to sell bonds; for the American government trying to sell treasuries, investor “adaptation” may come as a

nasty shock.

America’s economic debate is stuck in a time warp. On the one side, Mitt Romney’s conservative advisers defend tax cuts for the rich and spending cuts for the poor as if we had not just seen 30 years of failed Reaganomics. On the other, Paul Krugman defends crude Keynesianism as if we had learnt nothing in recent decades about the limitations of short-term fiscal stimulus. Both sides merely raise their decibel levels at each announcement of bad news.

The two sides live in timeless and increasingly irrelevant ideologies. The prescriptions peddled by the Republicans – slash taxes and spending, end financial and environmental regulations – are throwbacks to the 1920s. Today’s

free-market ideologues pay no heed to recent history, to the financial crisis of 2008 or to the devastating and ever more frequent climate shocks that threaten far more than the economy. Their single impulse is the libertarianism of the rich: the liberty to enjoy one’s wealth no matter what the consequences for society.

The other side is also wide of the mark. In Mr Krugman’s telling, we are in the 1930s – even though the collapse of output and rise of unemployment then was incomparably larger and different in character from today’s stagnation.

In his simplified Keynesian worldview, there are no structural challenges, only shortfalls in aggregate demand. There is no public debt problem. There is no global competitiveness challenge. Fiscal multipliers are predictable,

timeless, persistent and large. All growth reversals can be solved with

larger deficits. Politicians can be trusted to design short-term stimulus

spending programmes of hundreds of billions of dollars. Tax cuts are about

as good as increases in government spending, and short-term boosts in spending are about as good as longterm public investments. Not one of these conclusions stands scrutiny.

Why have we come to this empty debate that addresses none of the subtleties, trade-offs and uncertainties of the real situation? There are probably two main

reasons. First, the world is noisy and overloaded with media messaging.

Getting heard seems to require a short, sharp and exaggerated idea

endlessly repeated. Second, the world is facing novel problems at the global level, and novelty is hard to factor into economics, which is a rigid, ideological, theoretically based, and largely backward-looking field.

Here are some of the new problems of macroeconomic significance. First, the financial markets are global while regulation is at best national (and sometimes almost nonexistent or criminal).

This is killing the euro, but it is also undermining financial regulation and monetary policy everywhere. The US and UK are far more interested in defending

Wall Street and the City than in fixing global regulation. Germany has been much more interested in coddling its errant banks than in fixing the eurozone banking system.

Second, the world of work is being transformed. Low-skilled work is for offshore workers, immigrants or machines. In high-income countries, the only route to middle class jobs is through education, skills and active labour market policies that match

jobs and needs. Keynesian aggregate demand cannot create long-term employment for the low-skilled workers left to sink or swim in today’s globalised labour market.

Third, tax collections on the rich and capital income are becoming little more than a Swiss cheese of tax evasion and tax havens. Value added tax and payroll taxes can still be collected but capital income of all kinds increasingly escapes taxation.

These trends greatly exacerbate inequality of wealth and income.

Fourth, we are in the age of the Anthropocene, where global growth is limited by natural resources and climate change. If the world economy grows at 4 per cent or more, oil prices soar above $100 per barrel and food prices hit historic highs. This

fact is not yet properly part of any country’s economic strategy. America’s hydrofracking of natural gas and offshore drilling will not solve the heatwaves, floods, droughts and other disasters hitting much of the world this year. Nor will it do much to ease the resource constraints that will squeeze economic growth until we shift to new, sustainable technologies.

Fifth, the combination of falling tax collections and rising pension and healthcare costs poses long-term solvency challenges for most of our governments. These can be met only by new, long-term policy approaches. In short, we need new strategies to

overhaul broken systems of finance, labour markets, taxation, ecological management, budget management and investment incentives. Those challenges cannot be fixed through lowering taxes on the rich or higher fiscal deficits to create aggregate demand. New approaches must be long-term, structural, sensitive to

inequalities of skills and education, aligned with the need for more sustainable technologies and congruent with demographic trends.

It is time we moved beyond the Republican party economics of the 1920s and the Democratic party economics of the 1930s, to a new macroeconomics for the 21st century.

The writer is director of the Earth Institute at Columbia University

China’s Economy, Still Strong

THE “plum rain” that envelops Shanghai every summer — a confusing mix of drizzle, fog and smog — is a handy metaphor for the murkiness that currently enshrouds China’s economy.

A drumbeat of negative views about China’s economic prospects dominates the country’s image. The financial weekly Barron’s recently proclaimed in a cover story that “it looks like the Great China Growth Story may be falling apart.” On Friday, China is expected to announce new, subpar growth figures.

But consider a less prominent fact: a Bloomberg survey of economic forecasters yielded an average projected growth rate for China of 8.2 percent for 2012. If that’s the oft-predicted “hard landing” from the heights of China’s historic double-digit rates, let’s all wish for a similar fate for the United States. No other major country — not even Brazil or India — will grow at a rate near China’s this year.

As a China believer who recently made a return trip to the country after eight months, I was eager to assess whether the optimism evident there during my past visits had ebbed. I met with businesspeople and investors, mostly Chinese. To be sure, almost every meeting included an acknowledgment of relative soft spots in the economy and worries about things like declining exports, weakening Western economies, a housing bubble, too much investment and a failure to spur domestic consumption.

But on balance, the people I met were firmly optimistic that the fundamental “urge to surge” remained. If anything, the intervening decline in the Chinese stock market had made them more enthusiastic about investing.

“China wants you to misunderstand this economy,” one very successful investor said, suggesting that it serves China’s interests to be underestimated by the United States.

Concerns about China’s economy are often exacerbated by anxieties about its political stability amid a leadership transition, rampant corruption and official economic data of questionable veracity. But put those emotions and knee-jerk skepticism aside, and the economic picture looks rosy, at least to me.

Take, for example, China’s extraordinary investment rate of 48 percent of gross domestic product. High investment is a hallmark of an emerging economy; China’s capital stock per capita is still only about a tenth of the United States’, which suggests room for further investment.

All that spending gives China a feeling of lunging further and further into the 21st century. Visiting Pudong, Shanghai’s shiny new financial district, I recalled that when it was built, in the late 1990s, the vast project was ridiculed by critics as unlikely to ever be fully utilized. Today, Pudong is a major money center.

No doubt a portion of China’s investment has been misdirected. But misdirected overinvestment won’t bring down an economy; it simply represents lost consumption for Chinese families. In any event, I’d prefer some misdirected investment to the United States’ alternative: a modest 16 percent investment rate.

As for concerns about the housing market, here’s what passes for a burst bubble in China: a 2.2 percent decline in housing prices over nine months (and then a small increase in June). Compare that with the 33 percent drop in the United States between July 2006 and January 2012.

And what of the economic downturn in the West? Though it has indisputably hurt Chinese exports (which are still growing, albeit at a rapidly decelerating rate), China is now far less dependent on its exports; their share of G.D.P. has dropped from almost 40 percent in 2007 to 29 percent.

China may be totalitarian, but its leaders still behave as if they had 1.3 billion customers whom they need to keep happy by delivering steady and rapid progress up the economic ladder. Interest rates were cut in June and were just lowered again. Constraints on bank lending have been relaxed. The luxury tax was reduced. And notably, the managed appreciation of China’s currency over the past two years or so has been slightly reversed as China continues to pursue its neomercantilist strategy of manipulating everything from technology transfers to trade barriers.

While China has instituted only modest measures to stimulate consumer spending, the investors I met with are buying up businesses ranging from car dealerships to dairies, betting that the Chinese will step up their expenditures.

The “pessimists-lite” — those who argue that China’s growth rate may not re-accelerate — may be right. No economy can expand indefinitely at China’s historic double-digit rate. But for me, China’s economy still pulsates with the confidence of its growing entrepreneurial spirit, an important factor that doesn’t fit neatly into statistical models.

When asked to contribute to this series on the future of conservatism, I hesitated because it seemed to me that in both the US and Europe what was most needed was not a new form of conservatism but rather a reinvention of the left. For more than a generation we have been under the sway of conservative ideas, against which there has been little serious competition. In the wake of the financial crisis and the rise of massive inequality, there should be an upsurge of left-wing populism, and yet some of the most energised populists both in the US and Europe are on the right. There

are many reasons for this, but one of them is surely that publics around the world have very little confidence that the left has any credible solutions to our current problems.

The rise of the French Socialists and Syriza in Greece does not belie this fact; both are throwbacks to an old and exhausted left that will sooner rather than later have to confront the dire fiscal situation of their societies. What we need is a left that can stem the loss of rich-world middle class jobs and incomes through forms of redistribution that do not undermine economic growth or long-term fiscal health.

But if you can’t solve the problem from the left, maybe you can do it from the right. The model for a

future American conservatism has been out there for some time: a renewal of the tradition of Alexander Hamilton and Theodore Roosevelt that sees the necessity of a strong if limited state, and that uses state power for the purposes of national revival. The principles it would seek to promote are private property and a competitive market economy; fiscal responsibility; identity and foreign

policy based on nation and national interest rather than some global cosmopolitan ideal. But it would see the state as a facilitator rather than an enemy of these objectives.

Distrust of state authority has of course been a key component of American exceptionalism, both on the right and the left. The contemporary right has taken this, however, to an absurd extreme,

seeking to turn the clock back not just to the point before the New Deal, but before the progressive era at the turn of the 20th century. The Republican party has lost sight of the difference between limited government and weak government, reflected in its agenda of cutting money for enforcement capacity of regulators and the IRS, its aversion to taxes of any sort and its failure to see that threats to liberty can come from powerful actors besides the state.

A new kind of conservative might look at the presidency of Theodore Roosevelt for inspiration. Just as in the present, American capitalism in the late 19th century had generated powerful new interests, particularly the railroads and oil interests that provoked huge conflicts with farmers, shippers and their own workers. Roosevelt believed that no private interest should be more

powerful than the American state, and set about to ensure that by going after Northern Securities and other trusts. One imagines that if he had been president during the 2008-2009 financial crisis, he would not have been satisfied with the regulatory hodgepodge that is Dodd-Frank, but would have sought to break Goldman Sachs and JP Morgan Chase up into smaller pieces that could safely be allowed to go bankrupt if they took undue risks. If a new breed of conservatism could put Wall Street in its place, then it would have much more credibility taking on public sector unions and other interest groups on the left, just as Roosevelt did.

If contemporary conservatives could get over their ideological aversion to the state, they would

recognise that American government is both necessary and in great need of reform rather than abolition. Private sector companies have undergone huge changes in recent decades, flattening managerial hierarchies, upgrading workforce skills and experimenting ceaselessly with new organisational forms.

American government, by contrast, seems trapped in a late 19th-century bureaucratic model of rules and hierarchy. It needs to be smaller but also stronger and more effective. And this will not happen unless people see public service as a calling, rather than a despised occupation for people unable to make it in the private sector. In this regard, conservatives have an advantage because they can call people to public duty on the basis of the American nation rather than abstract ideals.

Recovery of strong-state conservatism would have important foreign policy consequences. It would

imply continuing investments in US military power and engagement in the world to maintain a balance of power favourable to American interests. This position is consistent, however, with a careful husbanding of national power: instead of undermining the American fiscal position through costly wars, it would see rebuilding of the economy as a precondition for a reassertion of military power over the long run.

Recovery of a Hamiltonian-Rooseveltian conservatism would require junking a lot of the ideas

that have animated the right since the rise of Ronald Reagan, such as the willingness to tolerate deficits as long as this meant lower taxes. But while this older tradition is in certain respects similar to strands of European conservatism, it is also profoundly American.

Both Hamilton and Roosevelt believed strongly both in the exceptional character of the American regime and in the idea of progress. Hamilton foresaw that a centralised state would be necessary

to create a national market, and an economy based on manufacturing. Roosevelt understood that the

industrial economy had unleashed forces that needed to be tamed. They saw national power as a tool

to achieve their ends, something to be nurtured and built rather than demonised as something to be

drowned in a bathtub.

How did you arrive at where you currently are in IR?

The most important political event in my lifetime has been what I call the world revolution of 1968. For me, it was a fundamental transformative event. I was at Columbia University when the uprising there took place, but that’s only a biographical footnote to what happened politically and culturally.

I’ve tried many times to analyze what happened exactly at that time, and what were its consequences, I’m convinced that 1968 was more important than 1917 (the Russian Revolution), 1939-1945 (the Second World War) or 1989 (the collapse of the Communisms in east-central Europe and the Soviet Union), years people usually point out as the crucial events. These other events were simply less transformative than the world revolution of 1968...

The revolution of 1968 brought, as you argued, the intellectual idea of centrist liberalism to an end. Since then, however, liberal capitalism has become even more deeply anchored in the world. How would you reflect on the changes the world has gone through in big lines referring to that point of view?

Before 1968, the ideology of what I call ‘centrist liberalism’ had dominated the intellectual, economic and political world for a good hundred-odd years, and had marginalized both conservative and radical doctrines, turning them into avatars of centrist liberalism. Now what happened in the world revolution of 1968 is that this automatic assumption that the only plausible view of the world was centrist liberalism was shattered and we returned to a world in which there are at least three major ideological positions: true conservatism, true radicalism, and the third is centrist liberalism which of course is still there – but now as one of three options rather than being considered the only viable intellectual position.

Now when you talk about ‘liberal capitalism’ you are referring to what is often called ‘neoliberalism,’ which is not at all the centrist liberalism that had dominated the world before. It is rather a form of conservatism. It has been pursuing a standard attempt to reverse the three trends that are negative from the view of world capital: the rising cost of personnel, the rising cost of inputs, and the rising cost of taxes. And neoliberalism – which goes under many names, including globalization – is an effort to reverse these trends and to reduce these costs. In this, it has been partially successful, but as all these attempts have shown (and I say ‘all’, because in the last five hundred years there have been quite a few), you can never push the costs back as low as they were previously. It is true that the costs of personnel, inputs, and taxes went up from 1945 to 1970 and have gone down from 1970 to, say, 2000, but they never went back down to the 1945 level. They went up two points and went back just one point. Now that’s a standard pattern in history.

I think the day of neoliberalism is absolutely at an end; its effectiveness is quite over. And globalization as a term and as a concept will be forgotten ten years from now because it no longer has the impact it was meant to have, which is to persuade everyone to believe Mrs. Thatcher’s preaching: ‘There is no alternative’. This was always an absurd statement, since there always are alternatives. But a large number of countries succumbed to it anyway, at least for a while.

The rhetoric about neoliberalism as the only way has now become clearly empty. Look at Europe – just look at President Sarkozy of France, who is clearly a protectionist. You won’t be able to give me the name of one European country willing to give up the subsidies to its farmers, because this is both politically totally impossible at the domestic level and completely contrary to the neoliberal logic. Mandelson wants to reduce subsidies at the European level, but he hasn’t got the necessary political support, which Sarkozy made very clear to him.

One has to distinguish between talk and reality. The reality is that European countries are not only protectionist, but they are increasingly protectionist and will be very much more so in the next ten years, as will Japan, China, Russia, and the United States. Alternating between protectionism and the free flow of factors of production has been a cyclical process for the last 500 years, and every 25 years or so we move from one direction to another, and right now we are moving back into a protectionist era.

A different view on climate change:

Pascal Bruckner

“The planet is sick. Man is guilty of having destroyed it. He must pay,” is how Bruckner caustically portrays the received wisdom on environmental “sin” and damnation in his latest book Le fanatisme de l’Apocalypse (The Fanaticism of the Apocalypse).

“Consider . . . the famous carbon footprint that we all leave behind us,” he writes in his introduction. “What is it, after all, if not the gaseous equivalent of original sin, of the stain that we inflict on our Mother Gaia by the simple fact of being present and breathing?”

Subtitled Sauver la Terre, punir l’Homme (Save the Earth, Punish Human Beings) the book rails against a peculiar Western malady. Yes, concerns about the environment are legitimate, Bruckner asserts, but catastrophisme is transforming us all into children “put in a panic in order to be better controlled”.

As the Jesuit-educated philosopher sees it, extreme climate change alarmism, with its warning bells chiming “The end of the world is nigh, repent ye”, represents a worrying new doctrine of ideological purity that even has totalitarian overtones.

Worst of all, Bruckner argues, these “political commissars of carbon” have “betrayed the best of causes” and turned the discourse of ecological terror into the “dominant ideology of Western society”.

Dividing his argument into three sections, provocatively titled “The Seduction of Disaster”; “The Anti-progress Progressives”; and “The Great Ascetic Regression”, Bruckner scorns the peddlers of the “propaganda of fear”.

“I do not attack ecology per se,” Bruckner says of his book. “I attack that degraded religion which emerges from it and turns into a culture of fear, hatred of progress and well-being.

“Why must we renounce all the joys of life under the pretext of global warming?”

The author’s special “passion” is, he says, Western guilt. Tears of the White Man, published in 1983, explored culpability regarding our colonial past, and in The Tyranny of Guilt, published in 2006, Bruckner examined the burdens of contemporary “penitence” about Western power and influence.

But as Bruckner judges it, a panic is now gripping Western elites, as they rapidly lose power amid the rise of countries like China, India and Brazil.

“Since we no longer dominate the world, we live in a permanent terror film and every day they [ecologists] explain to us that it is a miracle that we are still alive.

“The absurdity of this propaganda of fear – which recalls that of [former US president] George W. Bush regarding terrorism – is that we have never lived so long.

“We are living in a post-technological Middle Ages. Our mentality is that of the medieval peasant serf who sees maleficent forces in nature.

“Everything is dangerous. Simply to live has become an impossible task.

“We are afraid of everything – of mobile phones, of food, of dummies, of nappies, of antennas. We are living in a society which has a horror of risk and therefore is afraid of its own shadow.”

Intelligent responses to environmental degradation are therefore required rather than radical “belt-tightening” and “privation” in the form of a retreat from nuclear power and even domestic heating.

“There is this famous notion defended by the ecologists of ‘negawatts’: the best energy is that which we don’t expend,” the philosopher almost sneers.

“Yes, we need to make some savings. But wealth reproduces itself and life cannot simply be a subtraction. It is like saying ‘the best life is the life we don’t lead’. This is a kind of neo-Malthusianism.”

Bruckner detects suspicion about the merits of industrial progress not only in France but across the Western world, wherever extremist environmental politics has taken hold of public debate and even language.

The credo consists of saying to developing countries “stay poor because we became rich, we did evil to the planet and therefore everyone must impoverish themselves”.

“This discourse is a smokescreen to hide the anxiety of Westerners who have lost their supremacy in the world,” Bruckner retorts.

“Ecology is a means for us to say to these emerging countries ‘stay in the mud, remain broke, and moreover do not try to equal us because the industrial adventure is a failure’. In this sense the discourse is perfectly scandalous.”

"Meanwhile, the US academics, busying as usual with minute correlations, are still to catch up with the enormity of the task."

Economics as a "science" is no different than Sociology, Psychology, Criminal Justice, Political Science, etc.,etc.. To those in the "hard sciences" [physics, biology, chemistry, mathematics], these "soft sciences" are dens of thieves. Thieves who have stolen the "scientific method" and abused it.

These soft sciences all apply the scientific method to biased and insufficient data sets, then claim to be "scientific", then assert their opinions and biases as scientific results. They point to "correlations". Correlations which are made even though they know they do not know all the forces/factors involved nor the ratio of effect from the forces/factors.

They know their mathematical formulas and models are like taking only a few pieces of evidence from a crime scene and then constructing an elaborate "what happened" prosecution and defense. Yet neither side has any real idea, other than in the general sense, what happened. They certainly have no idea what all the factors or human behaviors were involved, nor the true motives.

Hence the growing awareness of the limitations of all the quantitative models that led to the financial crisis/financial WMDs going off.

Take for example the now thoroughly discredited financial and economic models that claimed validity through the use of the same mathematics used to make atomic weapons; Monte Carlo simulation. MC worked on the Manhattan Project because real scientists, who obeyed the laws of science when it came to using data, were applying the mathematics to a valid data set.

Economists and Wall Street Quants threw out the data set disciplines of science. The Quant's of Wall Street and those scientists who claimed the data proved man made global warming share the same sin of deception. Why? For the same reason, doing so allowed them to continue their work in the lab. They got to continue to experiment and "do science". Science paid for by those with a deep vested financial interest in the the false correlations proclaimed by these soft science dogmas.

If you take away a child's crayons and give him oil paints used by Michelangelo, you're not going to get the Sistine Chapel. You're just going to get a bigger mess.

If Behavioral Finance proves anything it is how far behind the other Social Sciences economists really are. And if the "successes" of the Social Sciences are any indication, a lot bigger messes are waiting down the road.

Centurion

Post a Comment